Connecticut VA Loans

Whether you receive PCS orders to relocate to Connecticut or are already a resident, purchasing a home can be a great financial move. Using a VA loan in Connecticut has many benefits for seasoned and first-time homebuyers alike.

With the average listing price of a home in Connecticut landing at $425,784, the VA loan’s signature $0-money-down benefit is a considerable advantage for Connecticut homebuyers.

See also: VA Loan Options for Other States

How to get a VA Loan in Connecticut

VA loans are made by private lenders and guaranteed by the Department of Veterans Affairs. Because private lenders make the loans and not the VA, you need to find a lender licensed in the state you plan to purchase or refinance.

For example, if you're purchasing a home in Bridgeport, CT, you'll need to find a lender licensed in Connecticut to do the loan.

Other Considerations for Getting a VA Loan in Connecticut

VA borrowers in Connecticut should also consider the cost and impact of VA loan limits and property taxes when making their home purchase.

Connecticut VA Loan Limits

VA borrowers in Connecticut with their full VA loan entitlement are not restricted by VA loan limits. This means you can borrow as much as a lender is willing to lend without needing a down payment.

However, veterans without their full VA loan entitlement are still bound to Connecticut VA loan limits.

As of January 1, 2026, VA loan limits for all counties in Connecticut are $832,750.

Property Taxes in Connecticut

Another consideration for VA buyers in Connecticut is property taxes. For certain VA buyers, there are exemptions.

You may be eligible for a property tax exemption in Connecticut if you meet one of the following conditions:

- If you are a veteran who has served at least 90 days of active duty and is honorably discharged, you may qualify for your town's standard property-tax exemption.

- If you are a veteran with a disability rating of 100%, you may receive a complete property tax exemption.

If you are required to pay property tax in Connecticut, the American Community Survey by the U.S. Census Bureau estimates you may pay the following in each county:

| County | Property Tax Rate |

|---|---|

| Capitol Planning Region | 2.14% |

| Greater Bridgeport Planning Region | 2.15% |

| Lower Connecticut River Valley Planning Region | 1.76% |

| Naugatuck Valley Planning Region | 2.04% |

| Northeastern Connecticut Planning Region | 1.54% |

| Northwest Hills Planning Region | 1.80% |

| South Central Connecticut Planning Region | 2.03% |

| Southeastern Connecticut Planning Region | 1.75% |

| Western Connecticut Planning Region | 1.47% |

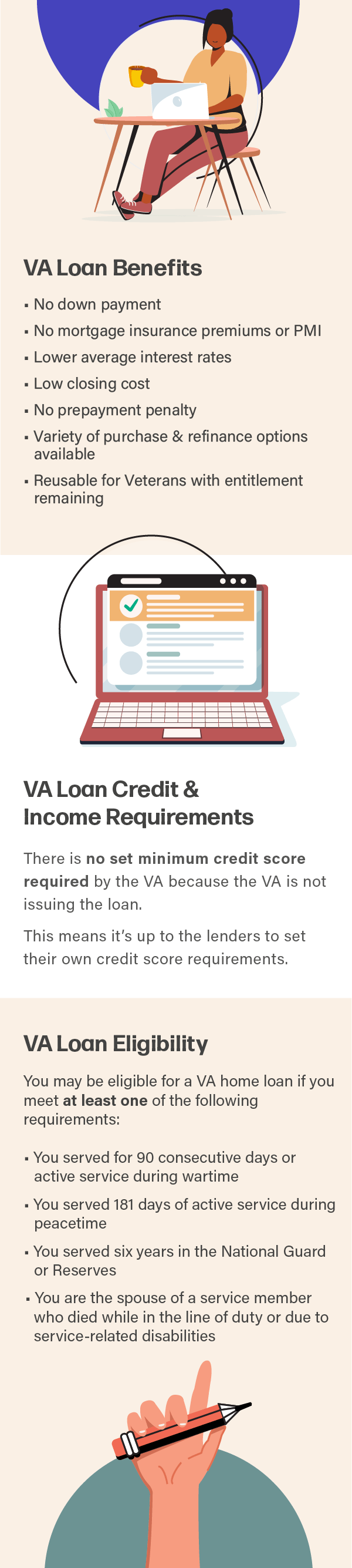

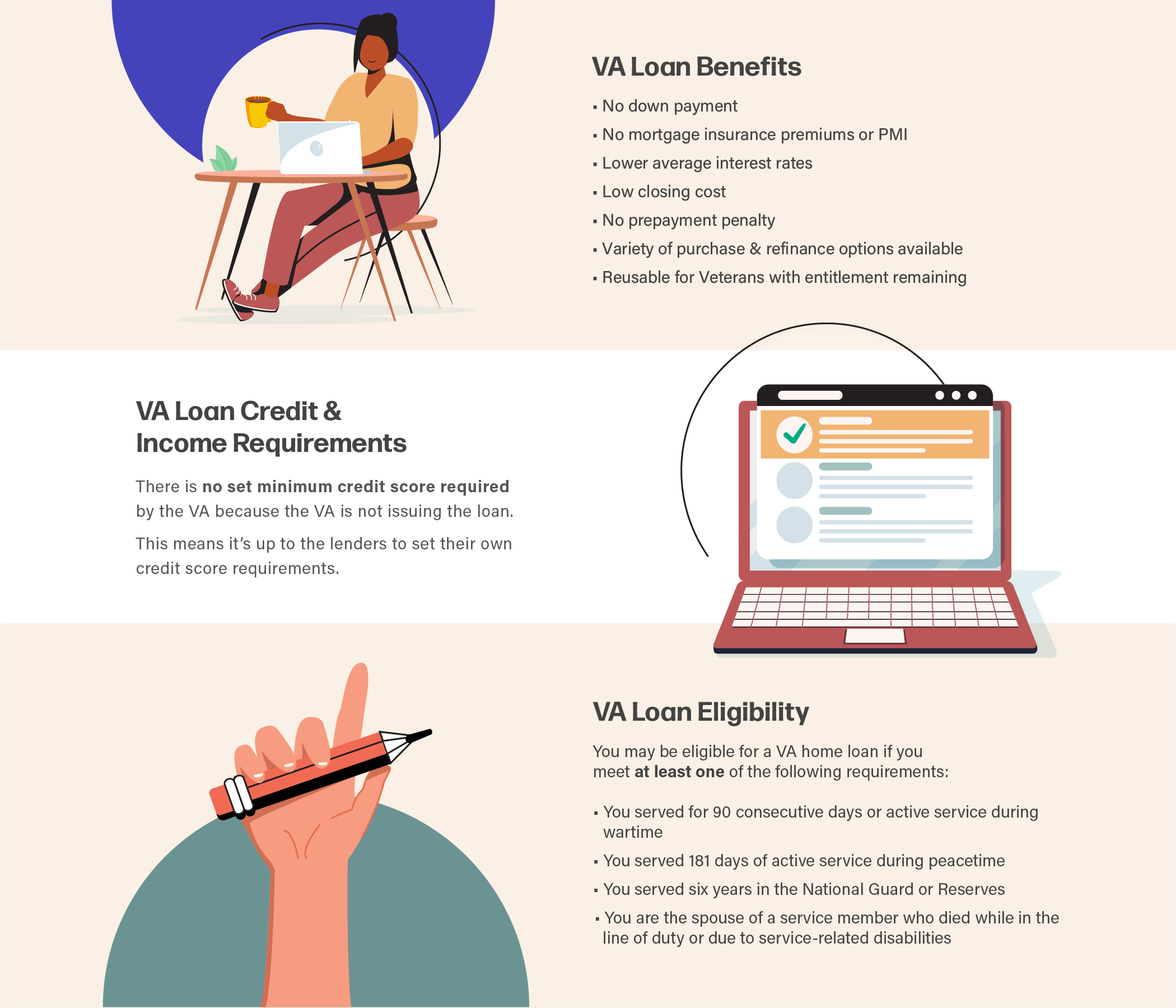

How VA Loans Work in Connecticut

View the graphic below to learn more about how VA loans work in Connecticut.