Vermont VA Loans

Deciding to purchase a house in Vermont is a huge financial decision, but with the unique benefits provided by the VA loan, your dream of homeownership just got that much easier.

With the average listing price of a home in Vermont landing at $387,631, the VA loan’s signature $0-money-down benefit is a considerable advantage for Vermont homebuyers.

See also: VA Loan Options for Other States

How to get a VA Loan in Vermont

VA loans are made by private lenders and guaranteed by the Department of Veterans Affairs. Because private lenders make the loans and not the VA, you need to find a lender licensed in the state you plan to purchase or refinance.

For example, if you're purchasing a home in Burlington, VT, you'll need to find a lender licensed in Vermont to do the loan.

Other Considerations for Getting a VA Loan in Vermont

VA borrowers in Vermont should also consider the cost and impact of VA loan limits and property taxes when making their home purchase.

Vermont VA Loan Limits

VA borrowers in Vermont with their full VA loan entitlement are not restricted by VA loan limits. This means you can borrow as much as a lender is willing to lend without needing a down payment.

However, Veterans without their full VA loan entitlement are still bound to Vermont’s VA loan limits.

As of January 1, 2026, VA loan limits for all counties in Vermont are $832,750.

Property Taxes in Vermont

Another consideration for VA buyers in Vermont is property taxes. For certain VA buyers, there are exemptions.

You may be eligible for a property tax exemption in Vermont if you meet one of the following conditions:

- A disabled veteran may receive an exemption of at least $10,000 on their primary residence if the veteran is 50 percent or more disabled as a result of service

- The exemption amount varies as each town votes on the amount

- The maximum exemption amount allowed by the state is $40,000

If you are required to pay property tax in Vermont, the American Community Survey by the U.S. Census Bureau estimates you may pay the following in each county:

| County | Property Tax Rate |

|---|---|

| Addison | 1.69% |

| Bennington | 1.71% |

| Caledonia | 1.83% |

| Chittenden | 1.61% |

| Essex | 1.69% |

| Franklin | 1.49% |

| Grand Isle | 1.36% |

| Lamoille | 1.67% |

| Orange | 1.75% |

| Orleans | 1.68% |

| Rutland | 1.86% |

| Washington | 1.87% |

| Windham | 1.87% |

| Windsor | 1.98% |

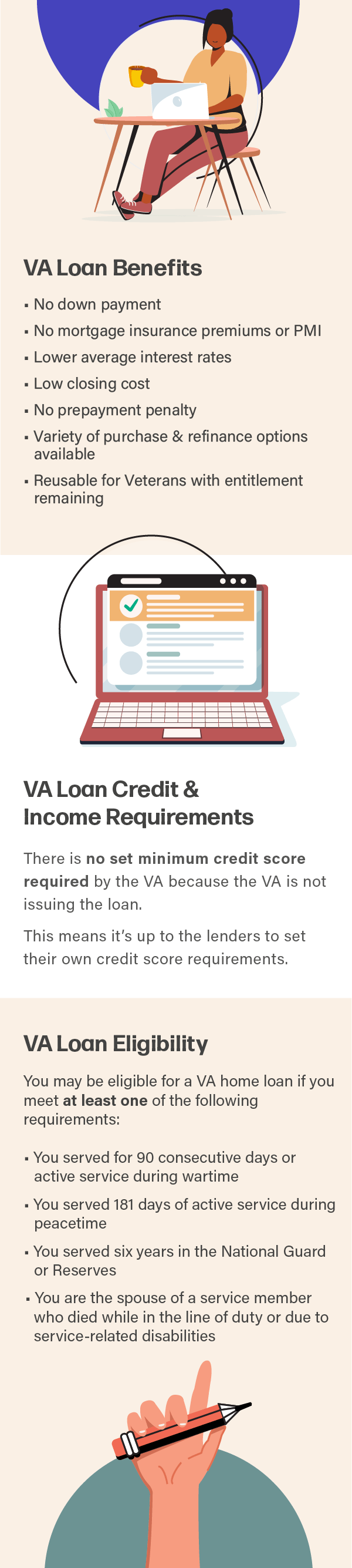

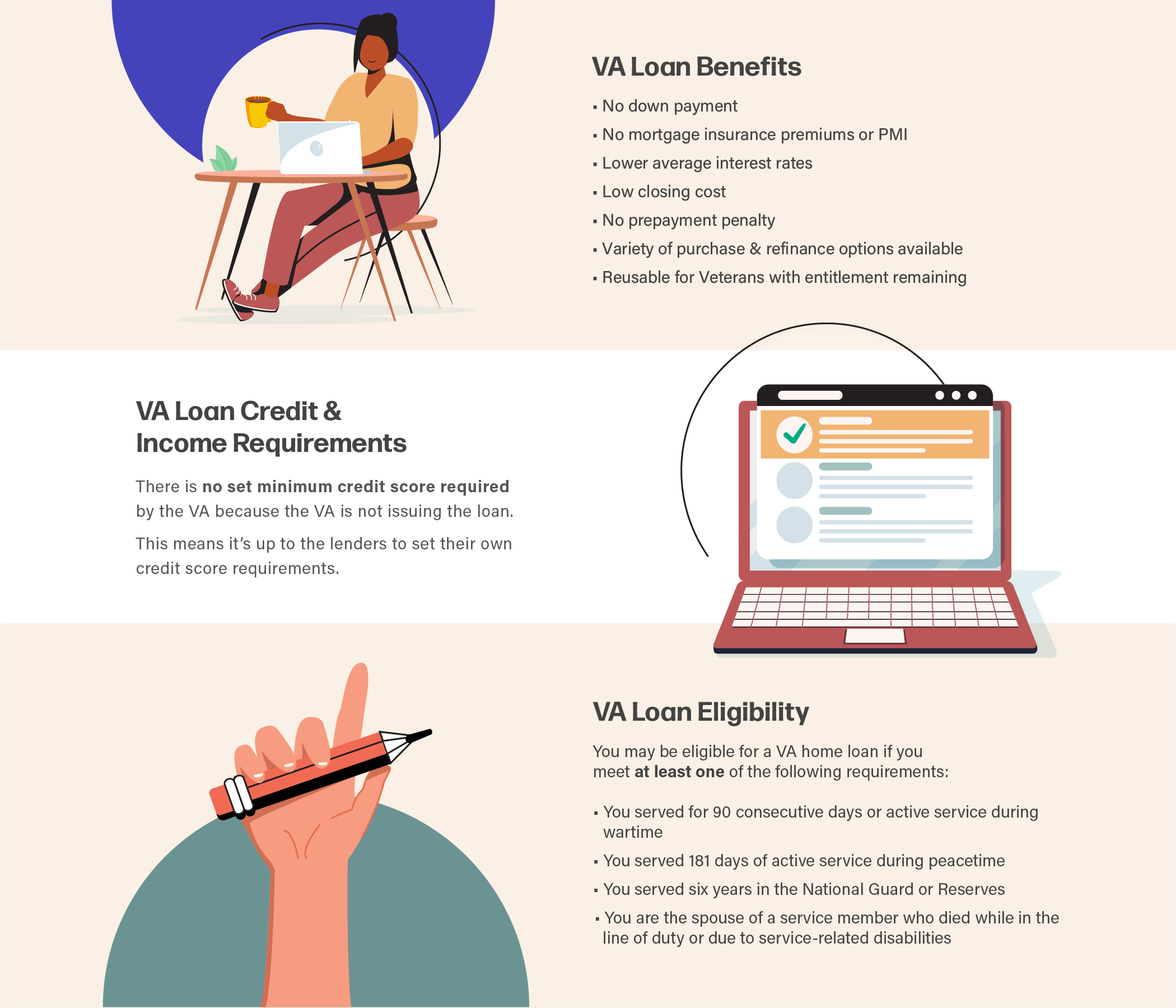

How VA Loans Work in Vermont

View the graphic below to learn more about how VA loans work in Vermont.